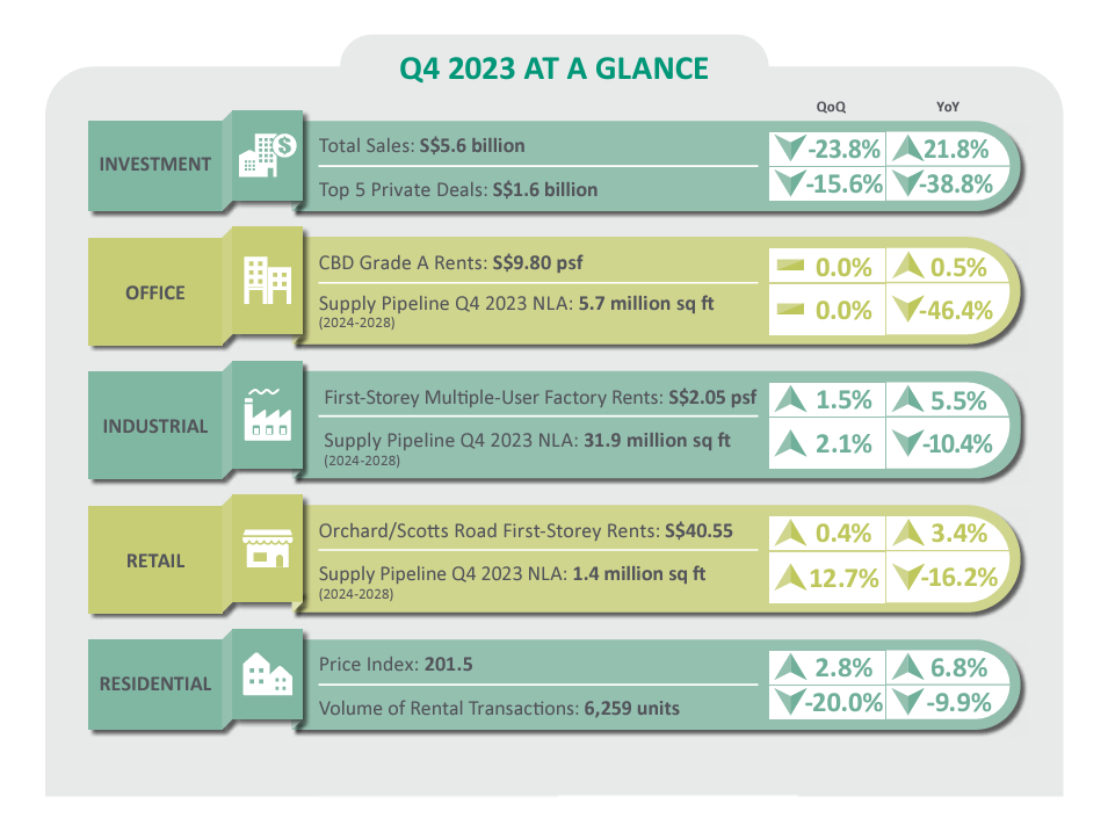

- Investment sales amounted to S$5.6 billion in Q4 2023, bringing the total investment sales for 2023 to S$20.4 billion. This represents a 29.4% decrease compared to the S$28.9 billion transacted in 2022.

- Government Land Sales (GLS) contributed S$7.8 billion in investment sales, which was a substantial increase of 40% compared to 2022’s S$5.5 billion. In contrast, the private sector saw a decline in investment sales by 45.8% to S$12.7 billion, down from the $23.3 billion recorded in 2022.

- As the economic recovery gains traction in 2024, investment activity in the office and retail sectors could pick up. Consequently, investment sales are expected to increase to S$25–28 billion in 2024.

- Islandwide net absorption increased from 445,000 sq ft in 2022 to 1,228,000 sq ft in 2023, driven significantly by the introduction of Guoco Midtown and demand for quality CBD office spaces.

- Office rents in Q4 2023 remained flat as most tenants are observed to favour lease renewals and rightsizing, instead of choosing to relocate.

- With the new supply of quality office spaces coming onstream in 2024, the office market will likely see an increase in relocation activity in the CBD area, as corporates remain interested in greener buildings in the mid to long term. We also expect more rightsizing of office space from the Technology sector to spur leasing activity.

- EDMUND TIE forecast a 0.3-0.5% growth for Premium and Grade A office rents in the CBD.

- In Q4 2023, warehouse rental growth picked up to 1.6% QoQ, from 1.5% in Q3 2023. FIrst-storey multiple-user factory rents posted a sharper growth of 1.5% QoQ in Q4 2023 from 1.0% in Q3 2023, as industrialists gradually took on space on the back of an improving manufacturing outlook.

- Industrial prices and rental indices continued its upward trajectory in Q4 2023, rising by 0.6% QoQ and 1.7% QoQ, respectively.

- We expect sustained overall industrial demand in 2024, on the back of a pickup in demand of factory space if the global semiconductor cycle turns around.

- With a surge in completions expected in 2024, rental growth is anticipated to moderate this year.

- Retail rents saw a moderate growth in Q4 2023. Prime first-storey rents rose by 0.4% to S$40.55 psf and S$33.75 psf in the Orchard/Scotts Road and Fringe/Suburban Areas micro-markets, respectively, while that in Other City Area micro-market remained flat at S$19.30 psf. Upper-storey rents across all areas remained unchanged.

- Retailers have experienced higher operating costs due to inflation and the geopolitical environment. The higher operating costs has led to brands grappling with market shifts and dynamics to face closures, while new-to-market retailers are expanding their market presence.

- We expect prime first-storey rental growth of between 3% and 5% for the Orchard/Scotts Road area in 2024. Prime first-storey rents in Other City Areas are expected to increase by 1-2%, while Fringe/Suburban Areas retail rents could increase by 2-3% in 2024.

- Total primary sales transaction volumes fell by 44% QoQ in Q4 2023 amid a limited number of launches. For the whole of 2023, primary home sales recorded a decline of almost 10% to 6,421 units, compared to the 7,099 units in 2022.

- On the back of the doubling of the ABSD rates for foreigners in April 2023, Q4 2023 witnessed a decline in the share of foreign buyers to 1.6%, down from 1.7% in Q3 2023. On a YoY basis, the share of foreign buyers declined to 3.5% in 2023 from 4.7% in 2022.

- Total private home rental transactions in Q4 2023 declined by 20% QoQ to about 18,800 units.

- Prices are likely to follow a slight positive trajectory in the coming months, as homebuying demand will be supported by an improving economic climate and a stable labour market.

- New home sales are expected to recover to around 7,000-8,000 units in 2024, from about 6,400 units in 2023. Secondary sale volume could moderate to 10,000-11,000 units this year, down from 14,791 units in 2022.

- Overall price growth is also expected to moderate to a more sustainable level of 3-5% in 2024, following 2023’s 6.7% growth.

END